Did you know that even the best traders can't predict the market with 100% accuracy—just like a weather forecast? In the world of trading, especially when it comes to reversal strategies, backtesting is essential. This article dives into the intricacies of backtesting, explaining what it is and why it matters. You’ll learn how to select the right platform, gather necessary data, and set up your backtesting environment effectively. We’ll also cover key metrics to analyze, common pitfalls to avoid, and techniques to enhance your strategy based on findings. With insights from DayTradingBusiness, you'll discover tools for automation, how to validate results, and even tackle slippage and transaction costs. Get ready to refine your trading approach and elevate your success!

What is backtesting in trading reversal strategies?

Backtesting in trading reversal strategies involves testing your strategy against historical market data to evaluate its effectiveness. You simulate trades based on past price movements to see how well your reversal signals would have performed. This process helps identify potential profitability and risk, enabling you to refine your strategy before applying it in real-time trading. To backtest effectively, use software or platforms that allow you to input your strategy criteria, analyze past performance, and adjust parameters for optimization.

Why is backtesting important for reversal strategies?

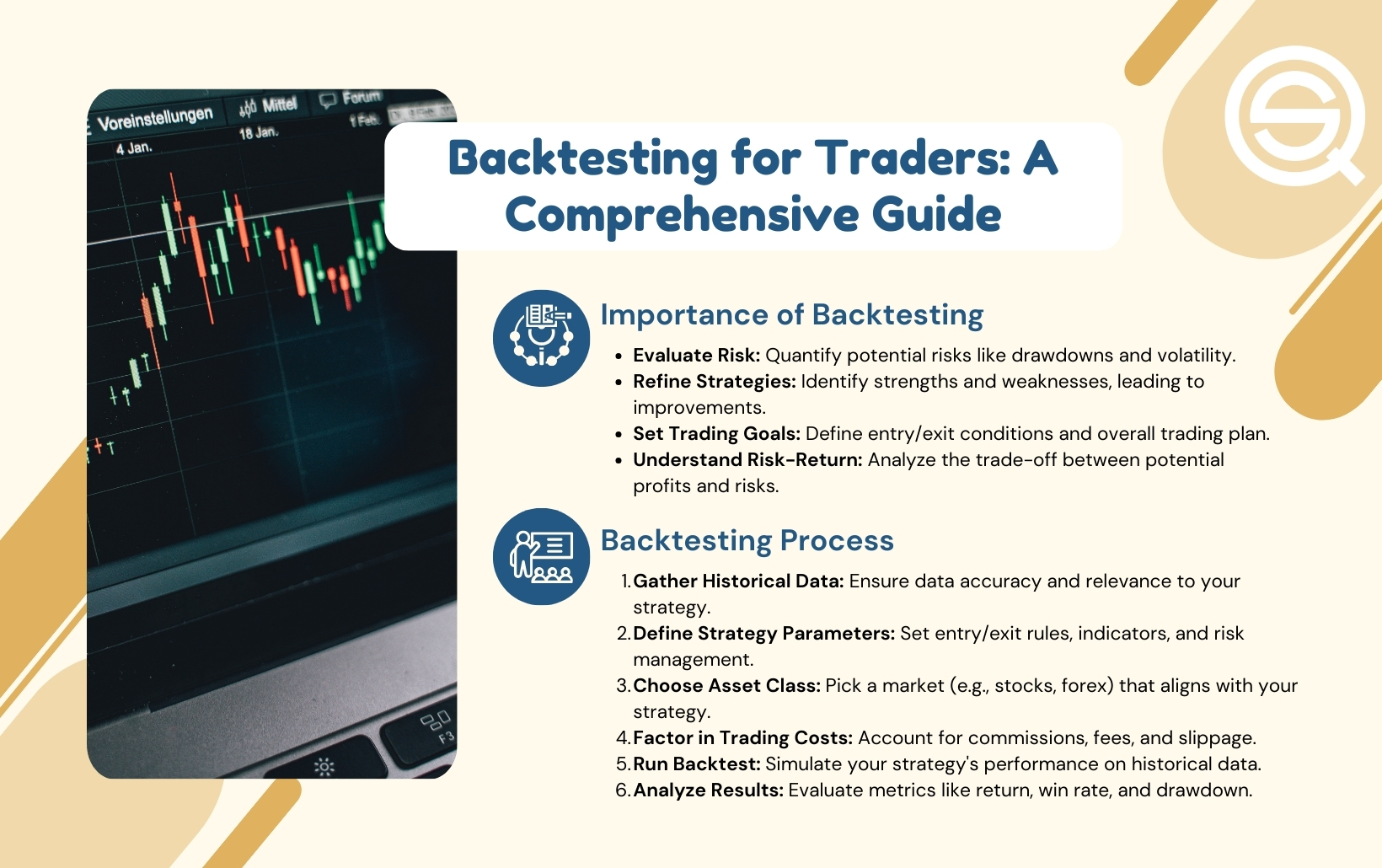

Backtesting is crucial for reversal strategies because it helps verify their effectiveness using historical data. It reveals how the strategy would have performed in different market conditions, allowing you to identify strengths and weaknesses. Through backtesting, you can fine-tune entry and exit points, adjust risk management, and build confidence in your approach before risking real capital. Overall, it ensures your reversal strategy is grounded in data, increasing the likelihood of success when implemented in live trading.

How do I choose a platform for backtesting?

Choose a backtesting platform by considering these factors:

1. User Interface: Look for an intuitive design that lets you navigate easily.

2. Data Availability: Ensure the platform provides access to quality historical data relevant to your reversal strategies.

3. Customization: Check if you can customize indicators and strategies to fit your specific needs.

4. Speed: Evaluate how quickly the platform processes backtests, especially for complex strategies.

5. Community and Support: A strong user community and good support can help you troubleshoot and improve your strategies.

6. Cost: Compare pricing models, including subscription fees or pay-per-use options.

Select a platform that aligns with your trading style and technical requirements for effective backtesting of your reversal strategies.

What data do I need for backtesting reversal strategies?

To backtest reversal strategies, you need historical price data, including open, high, low, and close prices. Additionally, volume data can provide insights into market activity. It’s also helpful to have data on indicators relevant to your strategy, like RSI or MACD, and any fundamental data that might affect price movements. Ensure your data spans various market conditions to test the strategy's robustness.

How can I set up my backtesting environment?

To set up your backtesting environment for reversal strategies, follow these steps:

1. Choose a Backtesting Platform: Use software like TradingView, MetaTrader, or Python libraries such as Backtrader or PyAlgoTrade.

2. Data Acquisition: Obtain historical price data for the assets you want to test. Ensure it includes open, high, low, close (OHLC) prices and volume.

3. Define Your Strategy: Clearly the criteria for your reversal strategy, including entry and exit points, stop-loss, and take-profit levels.

4. Code the Strategy: If using a coding platform, implement your strategy using the platform's scripting language. For no-code options, use visual tools to set up the logic.

5. Backtest Configuration: Set the time frame for your backtest, adjust parameters like slippage and commissions, and ensure your data is clean and formatted correctly.

6. Run the Backtest: Execute the backtest on your chosen platform, analyzing the results for win rate, drawdowns, and overall profitability.

7. Optimize Your Strategy: Adjust parameters based on backtest results to enhance performance, ensuring you avoid overfitting.

8. Analyze and Document: Review the results in detail, documenting insights and potential improvements for future testing.

By following these steps, you can effectively set up your backtesting environment for reversal strategies.

What metrics should I analyze during backtesting?

Analyze these key metrics during backtesting your reversal strategies:

1. Win Rate: Percentage of profitable trades to assess strategy effectiveness.

2. Profit Factor: Ratio of gross profit to gross loss, indicating overall profitability.

3. Maximum Drawdown: Largest peak-to-trough decline to evaluate risk.

4. Sharpe Ratio: Measures risk-adjusted return, helping you understand performance relative to volatility.

5. Average Trade Duration: Time each trade is held, which can provide insights into strategy execution.

6. Risk-Reward Ratio: Compares the potential profit of each trade to its potential loss, guiding position sizing.

7. Trade Frequency: Number of trades executed to gauge the strategy's activity level.

These metrics offer a comprehensive view of your strategy's viability and risk profile.

How do I interpret backtest results for reversal strategies?

To interpret backtest results for reversal strategies, focus on key metrics:

1. Win Rate: Assess the percentage of profitable trades. A higher win rate indicates effectiveness.

2. Risk-Reward Ratio: Analyze the average profit per winning trade compared to losses. Ideally, aim for a ratio above 1:2.

3. Drawdown: Examine the maximum drawdown to understand risk exposure. A lower drawdown signifies better risk management.

4. Trade Frequency: Look at the number of trades taken. Too few may indicate overfitting, while too many could suggest poor strategy.

5. Sharpe Ratio: Evaluate the risk-adjusted return. A higher Sharpe Ratio shows better performance relative to risk.

6. Consistency: Check if results are consistent across different market conditions to ensure robustness.

Use these metrics to gauge the viability of your reversal strategy and refine it as needed.

What common mistakes should I avoid in backtesting?

Avoid these common mistakes in backtesting reversal strategies:

1. Overfitting: Don’t tailor your strategy too closely to historical data. It may perform poorly in live trading.

2. Ignoring Transaction Costs: Always factor in slippage and commissions, which can skew results.

3. Cherry-Picking Data: Use a consistent dataset without selectively choosing periods that favor your strategy.

4. Lack of Robustness Testing: Test across different market conditions to ensure your strategy holds up under various scenarios.

5. Neglecting Out-of-Sample Testing: Validate your strategy on unseen data to better assess its performance.

6. Failing to Consider Market Impact: Understand that large trades may affect price, especially in less liquid markets.

7. Not Accounting for Risk Management: Incorporate stop-loss and position sizing rules to protect against significant losses.

By avoiding these pitfalls, you can enhance the reliability of your backtesting results.

How can I improve my reversal strategy based on backtesting?

To improve your reversal strategy based on backtesting, focus on these key steps:

1. Analyze Historical Performance: Review your backtesting results for win rates, profit margins, and drawdowns. Identify patterns in successful trades versus losses.

2. Refine Entry and Exit Points: Adjust your entry and exit criteria based on where historical reversals occurred. Consider using technical indicators like RSI or MACD to pinpoint better entry points.

3. Optimize Risk Management: Reassess your stop-loss and take-profit levels. Ensure that your risk-reward ratio is favorable based on backtested data.

4. Test Different Market Conditions: Backtest your strategy across various market conditions (bullish, bearish, sideways) to ensure robustness.

5. Incorporate Multiple Time Frames: Analyze reversals across different time frames to gain insights into potential entry and exit signals.

6. Utilize Monte Carlo Simulations: Run simulations to understand the variability and reliability of your strategy over time, helping you gauge potential future performance.

7. Seek Feedback and Iterate: Share your findings with a trading community or mentor. Use their insights to further refine your strategy.

Implementing these steps will enhance your reversal strategy based on backtesting results.

How Can I Effectively Backtest My Day Trading Reversal Strategies?

To backtest your reversal strategies, follow these steps:

1. **Select a Trading Platform**: Use software like MetaTrader or TradingView that supports backtesting.

2. **Gather Historical Data**: Obtain price data for the asset you want to test.

3. **Define Entry and Exit Criteria**: Clearly outline the conditions for entering and exiting trades based on your reversal strategy.

4. **Run Simulations**: Implement your strategy on historical data to simulate trades.

5. **Analyze Results**: Evaluate the performance metrics such as win rate, profit factor, and drawdowns.

6. **Adjust Strategy**: Refine your strategy based on the results and retest as needed.

Learn more about: Understanding Day Trading Reversal Strategies

Learn about How to Backtest Day Trading Strategies Effectively

What tools are available for backtesting reversal strategies?

Tools available for backtesting reversal strategies include:

1. MetaTrader 4/5: Popular for automated trading and backtesting with built-in strategy testers.

2. TradingView: Offers a user-friendly interface with Pine Script for custom backtesting.

3. Amibroker: A powerful tool for advanced users, allowing deep customization of backtesting strategies.

4. QuantConnect: A cloud-based platform for algorithmic trading, supporting C# and Python for backtesting.

5. Backtrader: An open-source Python library that provides flexible backtesting capabilities.

6. ThinkOrSwim: Allows users to backtest strategies using the paper trading feature.

7. NinjaTrader: A trading platform with strong backtesting features for various strategies.

8. TradeStation: Offers easy strategy development and extensive backtesting tools.

Choose based on your technical skills and specific strategy needs.

How do I validate my backtesting results?

To validate your backtesting results for reversal strategies, follow these steps:

1. Out-of-Sample Testing: Use a portion of your data that wasn't included in the backtest to see if the strategy holds up.

2. Walk-Forward Analysis: Continuously re-test your strategy on rolling time frames to ensure it adapts to changing market conditions.

3. Robustness Checks: Apply different market conditions, time frames, and asset classes to confirm consistency in results.

4. Statistical Measures: Analyze metrics like Sharpe ratio, drawdown, and win/loss ratio to assess performance qualitatively.

5. Slippage and Transaction Costs: Incorporate realistic slippage and trading costs into your model to see how they affect profitability.

6. Peer Review: Share your findings with other traders or analysts for feedback and validation.

7. Simulation of Market Impact: Consider how your trades may affect the market, especially in less liquid assets.

Following these steps ensures your backtesting results for reversal strategies are credible and actionable.

Can I automate my backtesting process?

Yes, you can automate your backtesting process for reversal strategies. Use trading platforms like MetaTrader, TradingView, or specialized software like Amibroker. Implement scripts or algorithms that simulate trades based on historical data. Ensure your code reflects your strategy's rules accurately and incorporates risk management parameters. This automation saves time and increases efficiency in testing multiple scenarios quickly.

What time frames are best for backtesting reversal strategies?

The best time frames for backtesting reversal strategies typically range from 1 hour to daily charts. Shorter time frames, like 15-minute or 30-minute, can provide quick signals, while daily charts offer a broader market perspective. Test across multiple time frames to find what fits your strategy best, considering the asset's volatility and your trading style.

How do I handle slippage and transaction costs in backtesting?

To handle slippage and transaction costs in backtesting your reversal strategies, incorporate realistic assumptions into your model. Estimate slippage by adding a fixed percentage to your entry and exit prices based on market conditions. For transaction costs, include commissions and fees for each trade.

Adjust your backtest results by subtracting these costs from your profit calculations to reflect a more accurate performance. Use historical data to gauge average slippage and costs for the assets you're trading. This way, you ensure your backtest reflects real-world trading scenarios.

What is the role of Monte Carlo simulations in backtesting?

Monte Carlo simulations in backtesting help assess the robustness of reversal strategies by generating a range of possible outcomes based on historical data. They allow traders to test how strategies would perform under various market conditions, accounting for randomness and uncertainty. By simulating different scenarios, including price movements and volatility, Monte Carlo simulations identify potential risks and the likelihood of achieving desired returns, enhancing strategy reliability before live trading.

How can I backtest reversal strategies across different markets?

To backtest reversal strategies across different markets, follow these steps:

1. Select Markets: Choose the markets you want to test, like stocks, forex, or commodities.

2. Data Collection: Gather historical price data for these markets, including open, high, low, and close prices.

3. Define Reversal Criteria: Clearly your reversal strategy rules, such as specific indicators or price patterns.

4. Use Backtesting Software: Utilize platforms like MetaTrader, TradingView, or Python libraries (e.g., Backtrader) to implement your strategy.

5. Run Simulations: Input your criteria and historical data into the software to simulate trades based on your strategy.

6. Analyze Results: Evaluate key performance metrics like win rate, profit factor, and drawdown to assess the effectiveness of your strategy.

7. Refine and Repeat: Adjust your strategy based on findings and retest to improve performance.

8. Consider Market Conditions: Test across different time frames and market conditions to ensure robustness.

This process will help you effectively backtest your reversal strategies in various markets.

Conclusion about How to Backtest Your Reversal Strategies

Backtesting your reversal strategies is a critical step in developing a successful trading approach. By utilizing the right tools and data, you can effectively analyze performance, avoid common pitfalls, and refine your strategies for better results. Remember to consider important metrics and account for factors like slippage and transaction costs. With proper validation and potential automation, backtesting can significantly enhance your trading confidence. For comprehensive guidance and resources, DayTradingBusiness is here to support you on your trading journey.

Sources:

- The long-run reversal in the long run: Insights from two centuries of ...

- Exploiting commodity momentum along the futures curves ...

- Analysis of market efficiency in main stock markets: using Karman ...

- A profitable trading algorithm for cryptocurrencies using a Neural ...

- Momentum crashes - ScienceDirect