Did you know that backtesting a trading strategy can be as thrilling as watching paint dry—until you find a winning pattern? In this article, we’ll explore the ins and outs of backtesting day trading patterns effectively. You'll learn what backtesting is and why it’s crucial for developing successful day trading strategies. We’ll cover how to select the right patterns, the best tools for backtesting, and essential data collection methods. Discover the optimal time frames for testing, how to interpret results, and common pitfalls to avoid. Plus, we’ll discuss strategy optimization, automation options, and the importance of risk management. By the end, you'll have a comprehensive understanding of how to refine your approach and validate your backtested results with live trading. Get ready to enhance your trading skills with insights from DayTradingBusiness!

What is backtesting in day trading?

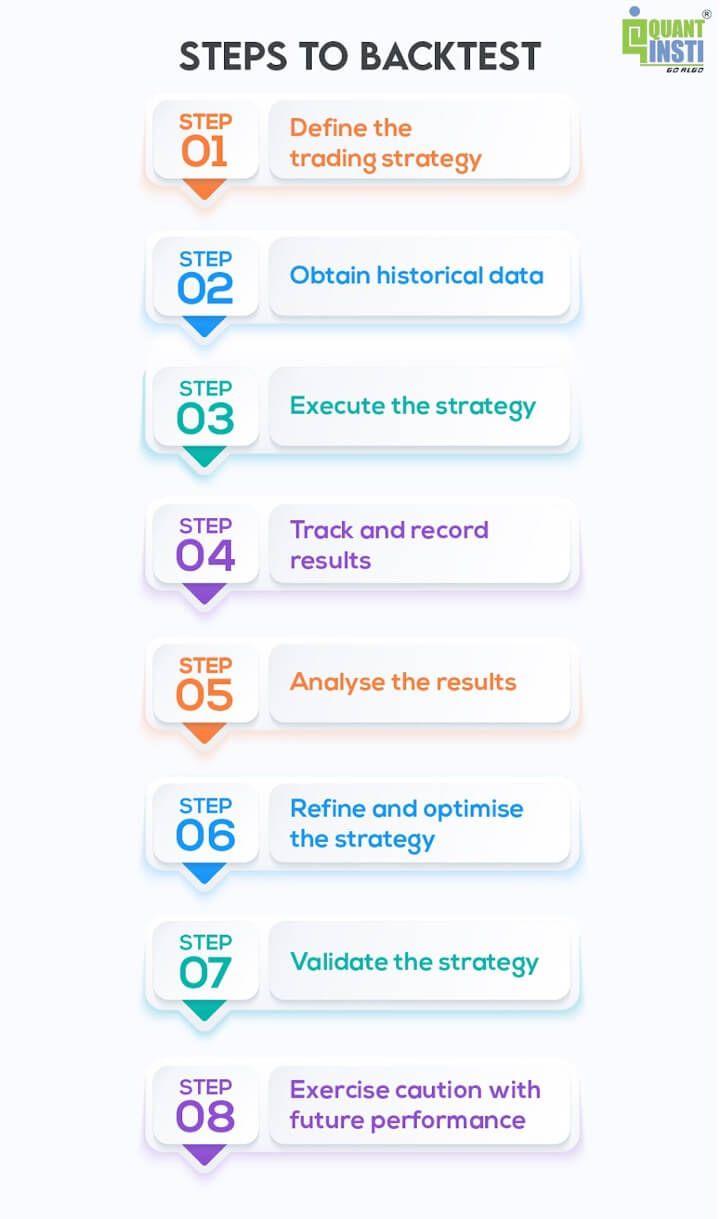

Backtesting in day trading involves testing a trading strategy against historical market data to evaluate its effectiveness. To backtest effectively, follow these steps:

1. Select a Strategy: Choose a specific day trading pattern or strategy, like scalping or momentum trading.

2. Gather Data: Use historical price data for the asset you want to trade. Ensure the data is accurate and covers enough time.

3. Set Parameters: Define entry and exit points, stop-loss levels, and profit targets based on your strategy.

4. Simulate Trades: Apply the strategy to the historical data, tracking each trade’s performance based on the parameters set.

5. Analyze Results: Look at metrics like win rate, average profit/loss, and maximum drawdown to assess the strategy’s viability.

6. Refine Strategy: Adjust parameters based on the results and retest to improve performance.

This process helps identify potential strengths and weaknesses before risking real capital.

Why is backtesting important for day trading strategies?

Backtesting is crucial for day trading strategies because it allows traders to evaluate the effectiveness of their strategies using historical data. By simulating trades based on past market conditions, traders can identify patterns, assess risk, and refine their entry and exit points. This process helps build confidence in a strategy before real money is put at risk. Effective backtesting reveals potential flaws, optimizes parameters, and enhances decision-making, ultimately improving overall trading performance.

How do I choose the right day trading patterns for backtesting?

To choose the right day trading patterns for backtesting, start by identifying patterns that align with your trading strategy, such as breakouts, reversals, or continuations. Use historical data to see which patterns have provided consistent results in the past. Focus on high-probability setups, like double tops or moving average crossovers, that fit your risk tolerance. Ensure you backtest over various market conditions to validate the patterns' effectiveness. Finally, keep track of performance metrics like win rate and risk-reward ratio to refine your selection.

What tools are best for backtesting day trading strategies?

The best tools for backtesting day trading strategies include:

1. TradingView: Offers advanced charting and scripting with Pine Script for custom strategies.

2. MetaTrader 4/5: Popular for forex trading, includes built-in backtesting features and extensive community support.

3. NinjaTrader: Excellent for futures and forex, featuring advanced backtesting and simulation tools.

4. Amibroker: Powerful for technical analysis and strategy formulation, with detailed backtesting capabilities.

5. QuantConnect: A cloud-based platform that supports C# and Python for algorithmic trading and backtesting.

6. Thinkorswim: Provided by TD Ameritrade, it offers tools for backtesting strategies with historical data.

Choose based on your specific trading needs and the markets you focus on.

How do I collect data for backtesting day trading patterns?

To collect data for backtesting day trading patterns, follow these steps:

1. Choose a Data Source: Use platforms like Yahoo Finance, Google Finance, or specialized services like Quandl for historical stock data.

2. Select Timeframe: Focus on minute-level or hourly data for day trading. Ensure you have at least a few months of data for accurate analysis.

3. Gather Price Data: Extract open, high, low, close (OHLC) prices, and volume for the selected stocks.

4. Utilize APIs: If you're tech-savvy, use APIs from services like Alpaca or Interactive Brokers to automate data collection.

5. Consider Additional Indicators: Gather data on technical indicators such as moving averages or RSI if they are part of your trading strategy.

6. Clean and Format Data: Make sure the data is clean and structured in a way that your backtesting software can read it.

7. Store Data: Organize the data in a database or spreadsheet for easy access during backtesting.

By following these steps, you'll have the necessary data to effectively backtest your day trading patterns.

What time frames should I use for backtesting day trading?

For backtesting day trading, use time frames like 1-minute, 5-minute, and 15-minute charts. These allow you to capture short-term price movements and identify patterns effectively. Additionally, consider using daily charts for broader trend analysis. Test strategies over at least 6 months to a year to gather sufficient data, adjusting as necessary based on market conditions.

How can I interpret backtesting results effectively?

To interpret backtesting results effectively, focus on these key aspects:

1. Win Rate: Analyze the percentage of profitable trades. A higher win rate indicates a potentially successful strategy.

2. Risk-Reward Ratio: Evaluate how much you gain on average for each dollar risked. A ratio above 1:1 is desirable.

3. Drawdown: Check the maximum drawdown to understand potential losses during unfavorable periods. Lower drawdowns indicate better risk management.

4. Trade Frequency: Consider how many trades were executed. A strategy that trades too frequently may incur higher transaction costs.

5. Sharpe Ratio: Use this to assess risk-adjusted returns. A higher Sharpe ratio suggests more effective performance relative to risk taken.

6. Consistency Over Time: Look for stable performance across different market conditions and time frames to ensure reliability.

7. Parameter Sensitivity: Test how changes in strategy parameters affect results. Stable results indicate robustness.

By focusing on these elements, you can derive actionable insights from your backtesting results for day trading patterns.

What common mistakes should I avoid when backtesting?

1. Ignoring Slippage and Commissions: Always factor in transaction costs and slippage to get realistic results.

2. Overfitting: Avoid tailoring your strategy too closely to historical data. It can lead to poor performance in live trading.

3. Using Incomplete Data: Ensure you have comprehensive data, including different market conditions, to avoid bias.

4. Not Accounting for Market Impact: Be mindful that large trades can affect market prices, especially in less liquid stocks.

5. Failing to Validate Results: Test your strategy on out-of-sample data to confirm its effectiveness.

6. Neglecting Risk Management: Implement proper risk management rules during backtesting to mirror real trading conditions.

7. Overlooking Psychological Factors: Consider how emotional responses to losses might affect your strategy's execution in real life.

8. Relying Solely on Historical Performance: Past performance doesn’t guarantee future results; stay adaptable to changing market dynamics.

How do I optimize my day trading strategies after backtesting?

To optimize your day trading strategies after backtesting, follow these steps:

1. Analyze Results: Review your backtest data to identify winning and losing trades. Look for patterns in entry and exit points.

2. Refine Parameters: Adjust your strategy parameters based on the backtest findings. Experiment with different indicators, timeframes, and stop-loss levels.

3. Risk Management: Ensure you're applying proper risk management techniques. Set maximum loss limits and adjust position sizes accordingly.

4. Diversification: Test your strategies across multiple securities or markets to see where they perform best. This can enhance overall performance.

5. Continuous Testing: Implement forward testing in a simulated environment to validate your optimized strategy in real-time conditions before going live.

6. Feedback Loop: Regularly revisit and update your strategy based on new market conditions or additional data from future backtests.

7. Keep Learning: Stay updated on market trends and continue educating yourself on new strategies and techniques.

By systematically refining your approach, you can enhance your day trading performance and adaptability.

Can I automate the backtesting process for day trading?

Yes, you can automate the backtesting process for day trading. Use trading platforms like MetaTrader, TradeStation, or NinjaTrader, which offer built-in tools for scripting and automation. Write algorithms that define your trading strategies, including entry and exit points. Utilize historical price data to test your strategies over various time frames. This allows you to evaluate performance metrics like win rate and drawdown automatically. Implementing this can save time and help refine your day trading patterns effectively.

Learn about How to Automate Your Day Trading Backtesting Process

How do I validate my backtested results with live trading?

To validate your backtested results with live trading, start by implementing a small-scale live trading strategy using the same parameters as your backtest. Monitor your trades closely to see if they align with your backtested outcomes. Keep a detailed trading journal to track performance metrics and compare them with your backtested data. Adjust for market conditions since they can differ from historical data. Finally, consider using a demo account to test your strategy in real-time without financial risk before scaling up.

What are the limitations of backtesting in day trading?

Backtesting in day trading has several limitations. First, it relies on historical data, which may not predict future performance. Next, it often overlooks market conditions like slippage, liquidity, and transaction costs that can impact results. Additionally, overfitting can occur, where strategies perform well on past data but fail in real-time trading. Lastly, psychological factors are not accounted for in backtesting, which can affect decision-making under pressure.

How often should I backtest my day trading strategies?

You should backtest your day trading strategies regularly, ideally after each significant market change or after you've made adjustments to your strategy. At a minimum, backtest quarterly to ensure your strategies remain effective. Frequent testing helps you adapt to market conditions and refine your patterns for better performance.

Learn about How Do Prop Firms Affect Day Trading Strategies?

What is the role of risk management in backtesting?

Risk management in backtesting is crucial for evaluating the viability of day trading patterns. It helps identify potential losses, set stop-loss levels, and determine position sizing. By incorporating risk parameters, traders can assess how strategies perform under various market conditions, ensuring they’re not just profitable but also sustainable. This approach minimizes emotional decision-making and enhances discipline, leading to more reliable trading outcomes. Ultimately, effective risk management during backtesting allows traders to refine their strategies and improve their overall performance.

How can I refine my backtesting approach over time?

To refine your backtesting approach for day trading patterns, start by clearly defining your trading strategy and the specific patterns you want to test. Use historical data that aligns with your strategy's timeframe, ensuring it's clean and relevant.

Regularly update your data sets and incorporate various market conditions to assess performance across different scenarios. Analyze the results critically; look for patterns in your successes and failures.

Adjust your parameters based on findings, and don’t hesitate to tweak your strategy as you learn. Implement a systematic approach to track your changes and their impacts over time. Lastly, consider using advanced tools or software that can automate parts of your backtesting to improve efficiency and accuracy.

What are some successful day trading patterns to backtest?

Successful day trading patterns to backtest include:

1. Breakouts: Look for stocks that surge past resistance levels with high volume.

2. Reversals: Identify price action at support or resistance zones indicating a potential trend reversal.

3. Flags and Pennants: These continuation patterns signal short-term pauses in a trend before a breakout.

4. Moving Average Crossovers: Test the effectiveness of short-term moving averages crossing above or below long-term averages.

5. Gap and Go: Analyze stocks that gap up or down at market open and continue in that direction.

6. Candlestick Patterns: Patterns like hammer, engulfing, or doji can provide insights into market sentiment.

Backtest these patterns using historical price data, focusing on entry and exit points to evaluate their profitability and risk.

Conclusion about How to Backtest Day Trading Patterns Effectively

In summary, effective backtesting is crucial for developing robust day trading strategies. By selecting the right patterns, utilizing appropriate tools, and interpreting results accurately, traders can significantly enhance their decision-making process. Avoiding common pitfalls and integrating risk management will further strengthen your approach. Regularly refining your methods and validating your findings with live trading will ensure continued success. For deeper insights and guidance, DayTradingBusiness is here to support your trading journey.

Learn about How to Backtest Day Trading Strategies Effectively